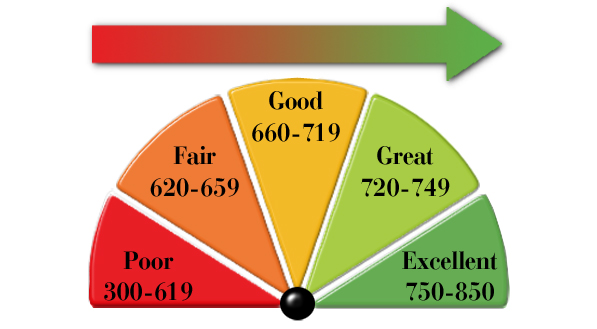

Want a credit score as high as 720, or even higher?

Your "credit score" is everything.

It determines what you pay on a whole lot of things, like mortgages, car loans, personal loans, and even utilities and insurance. Your "credit score" is everything. Let's make sure it's a good one.

Unhappy with your credit score?

Hate getting turned down for credit? Hate not getting the stuff you want?

"Wanna get what you want when you want it?"

Want a higher credit score?

Want a credit score as high as "720"...or even higher?

Then...the truth is...you may need to "START" WITH A BANKRUPTCY.

We figured it out. We figured out how you can use bankruptcy to "kickstart" your credit score to a much higher level. Let me explain.

The secret is to get back to paying all your bills “ON TIME” every month, month in, month out.

The truth is that paying your bills “on time” is now...and has always been...the key to a high credit score.

"According to FICO data, a 30-day delinquency could cause as much as a 90 to 100 point drop...for a consumer who has never missed a payment on any credit acount." (According to Equifax Finance Blog, 2/7/14, see "Credit" tab)

Can’t afford to pay your bills “on time”? I understand.

If you could pay all your bills “on time”, you probably wouldn’t be reading this page.

Likely, you are here reading this because you have more bills than you can pay.

If so, you are in good company. Times are tough.

And, it goes without saying that if you have more bills than you can pay, you have either not been paying on some bills, or you have been sending your payments in late.

Paying late or not at all is what hurts your credit score the most.

Most people think that filing bankruptcy will hurt their credit. The truth is that, for the most part, bankruptcy is not what hurts your credit score.

The truth is that "not paying your payments 'on-time' is what hurts your credit score".

And...in most cases..."not paying your payments on-time" started long before you even thought about calling a bankruptcy attorney. By the time you call a bankruptcy attorney's office...likely...the damage is already done.

Think about it. If you had a great credit score, you wouldn't need to call a bankruptcy attorney. And if the damage is already done, how can bankruptcy hurt it?

Not making your payments "on-time" is what hurts your credit score. And every month, month-in, month-out, you send in payments late (or not at all) is one more month your credit score takes a hit like a hammer blow to a plate-glass window.

Want to change all that?

Want to improve your credit score?

Want to give yourself at least the opportunity to work toward a credit score as high as 720...or even higher?

Then, the first step is to get yourself back into a position where you can make your payments “on time”, month-in, month-out, and forever.

And, that’s where bankruptcy comes in.

The truth is that filing bankruptcy may be the best thing that ever happened to your credit score.

Let me repeat that.

Filing bankruptcy may be the best thing that ever happened to your credit score.

Why?

Because bankruptcy eliminates debts you CAN'T afford. Very simply, bankruptcy gets rid of debt. That's what it does.

And when you get rid of debts you CAN'T afford, what's left? Answer: The bills you CAN afford.

And, if all you have left are bills you CAN afford, you can get back to paying them “on time”.

That's the key to a great credit score. Paying your bills "on-time".

Want the opportunity to work toward a higher credit score, perhaps much higher, perhaps as high as 720, or even higher?

Start with a bankruptcy.

Think of it this way. Bankruptcy: “The backdoor to a high score”.

Here's another way to look at it:

Bankruptcy: The "reset" button for your credit score.

“Ok, ok, so first I use bankruptcy to get rid of the debts I can’t afford, so that I can get back to paying the rest of my bills ‘on time’."

"But, what then?”

Good question. Here's the answer:

Start paying the rest of your debts and bills ‘on-time” every month. This alone will raise your credit score.

Then...with your credit score on the rise...you will be ready...ready to take the simple steps necessary to start building a higher and higher credit score, hopefully as high as 720...and...over time...even higher.

If others can do it, you can too. It's not hard. You just have to take the right steps and continue taking the right steps.

The secret is to learn what steps to take but, perhaps even more important, what steps NOT to take. We can point you in the right direction. When your bankruptcy is finished, all you have to do is ask and you can get started.

And, remember this. You don't have to go it alone, and you don't have to figure out what to do. There are experts available to you, experts who make it their business to help people, like you, rebuild credit and increase their credit scores.

But, remember, the necessary first step in the process is to get rid of the debts you cannot afford, so you can get back to paying the rest of your bills "on-time".

That’s what bankruptcy is for. That’s what bankruptcy does best.

If you don’t take this first step, then nothing else matters.

People who continue to make "late"payments don’t ever get to have or enjoy a great credit score. That's just the truth.

Want to start re-building your credit and increasing your credit score?

First, you have to get back to making your payments "on-time" every month, month-in, month-out.

Want to give yourself a chance to increase your credit score, a chance to increase it to as high as 720, or even higher?

You need to get rid of the bills you CAN'T AFFORD.

Start with a bankruptcy.

Bankruptcy...the fastest way...under the law...to get rid of bills you CAN'T AFFORD.

If filing bankruptcy is right for you...hopefully...you will be well on your way to...obtaining the credit score you want,...getting the respect you deserve, and...once again...feeling like the person in control, rather than someone banks and credit card companies bounce around and treat as just another number.

Want to at least give youself a chance to see what it feels like to be a member of the “720" club?

If so, it's in your best interest to set up a consult with an experienced bankruptcy to see if filing bankruptcy is right for you.

What's more, you should be able to get ALL the information you need FOR FREE. Most bankruptcy attorneys provide a totally FREE and totally confidential Initial Consultation.

In the meantime, keep this in mind: If filing bankruptcy is right for you, “the faster you file...the faster you smile”.

Rebuild your credit...Rebuild your life.

Note: This page was written by and is included here with the permission of Shawn Orcutt, bankruptcy attorney and credit expert, who is dedicated to providing you the information you need to re-build your credit score AFTER bankruptcy.

Click here to download a FREE copy of Shawn's amazing book entiitled: Credit Scores Keys: How To Rebuild Your Credit Score After Bankruptcy.

Message from the Law Offices of John T. Orcutt

Call us and let’s see if filing bankruptcy is right for you.

Day or night, 7 days a week, just call toll free: +1-833-627-0115.

The consultation is totally FREE. Get the answers you need. Find out all your options, bankruptcy and otherwise. Find out how much debt you can get rid of...hopefully enough to let you can get back to paying the rest of your bills "on-time".

We're here to help. Call us.

IMPORTANT NOTICE TO PROSPECTIVE CLIENTS FROM THE LAW OFFICES OF JOHN T. ORCUTT:

Any reference to your present or future credit record, credit history, credit rating or credit score in our advertising or during consultation with our law firm or during the handling of your bankruptcy case (if filing bankruptcy is right for you) is provided for the sole purpose of either: (1) discussing and properly counseling and advising you on the interrelationship between and possible impact of filing bankruptcy on your credit record, credit history, credit rating and/or credit score, (2) advising and counseling you with respect to the proper handling and preparation of your bankruptcy case (again, if filing bankruptcy is right for you), or (3) pointing out the huge “ancillary” credit-score-related benefit of filing bankruptcy caused by using the bankruptcy laws to get rid of debts you can’t afford so that, hopefully, you can get back to paying the rest of your debts “on-time”.

We are bankruptcy attorneys. We know bankruptcy. We are not experts in credit repair or credit score rebuilding. We don't provide credit repair or credit score rebuilding services. The money you pay or agree to pay our law firm is solely: (1) for the purpose of providing you the counsel, advise and services necessary for you to make the decision whether or not to file bankruptcy and (2) for the purpose of getting your bankruptcy case prepared, filed and properly handled.

Our law firm does not, and will not, sell, provide or perform any service, nor take any action, for the express or implied purpose of: (1) improving your credit record, credit history, credit rating or credit score, or (2) providing you advice or assistance with regard to improving your credit record, credit history, credit rating or credit score. If you want these other types of non-bankruptcy-related services, you would need to hire some other person or organization who provides such services.

In this regard, as an accommodation to you, without cost to you, and for the purpose of steering you in the right direction and because we know how important your credit score is to your financial future, we will try to provide you with pamphlets, handouts, and webpage content, which contain information about persons and organizations that provide such services and also helpful and instructive information and/or links to information created by such other persons or organizations.

THE LAW OFFICES OF JOHN T. ORCUTT, P.C.

We are a debt relief agency. We help people filed for bankruptcy relief under the United States Bankruptcy Code.

Debts Hurt! Got debt? Need help? Get started below!

Serving All of North Carolina

- Bankruptcy Attorneys Raleigh NC (North)

- Bankruptcy Attorney Fayetteville NC

- Bankruptcy Attorney Durham NC

- Bankruptcy Attorneys Wilson NC

- Bankruptcy Attorneys Greensboro NC

- Bankruptcy Attorneys Southport NC

- Bankruptcy Attorneys Wilmington NC

Bankruptcy Attorneys Raleigh NC (North)

6616 Six Forks Rd #203 Raleigh, NC 27615 North Carolina

Tel: (919) 847-9750

")

Bankruptcy Attorney Fayetteville NC

2711 Breezewood Ave Fayetteville, NC 28303 North Carolina

Tel: (910) 323-2972

Bankruptcy Attorney Durham NC

1738 Hillandale Rd Suite D Durham, NC 27705 North Carolina

Tel: (919) 286-1695

Bankruptcy Attorneys Greensboro NC

2100 W Cornwallis Dr. STE O Greensboro, NC 27408 North Carolina

Tel: (336) 542-5993

Bankruptcy Attorneys Southport NC

116 N Howe St. Suite A Southport, NC 28461 North Carolina

Tel: (910) 218-8682

Bankruptcy Attorneys Wilmington NC

116 N. Howe Street, Suite A Southport, NC 28461 North Carolina

Tel: (910) 447-2987